High-yield bonds should continue to yield attractive returns in 2024. Capital Four’s René Kallestrup advocates a selective approach with a view to sectors and regions.

High-yield bonds had a very good year in 2023. While the general bond market rose by 5.3% last year according to Morningstar, high-yield bonds performed on average by 12.1%1. According to René Kallestrup, one of the portfolio managers of Nordea’s European High Yield Bond and Flexible Credit Strategies, decent returns are likely to continue in the current year (although not as high as last year).

One reason for this is yield of the portfolio, shorter duration of the asset class and pull-to-par with bonds trading around 95 compensating for expected defaults. After peaks of credit spreads in 2020 and 2022, they have tightened again and currently offer high 300 basis points in Europe and a low 300 basis points in the USA2. Kallestrup therefore prefers European high-yield bonds to their US counterparts based on the current expected path of defaults. He also considers the rating composition on the European market to be advantageous.

More defaults expected in the USA

Default rates remain at average historical levels. Although they have risen again from extremely low levels in 2021 and 2022 to just over 2% because of the economic slowdown and idiosyncratic events3, Kallestrup does not expect default rates to shoot up sharply in the coming quarters – unless there is a deep recession. Default rates in the USA should be at a higher level than in Europe. While JP Morgan expects default rates of 2.5% in Europe and 2.75% in the USA for high-yield bonds over the next twelve months4, Capital Four expects lower default rates in Europe (1.8%) and higher rates in the USA (2.9%). The reason for the higher default forecast for the US high-yield market is the larger proportion of bonds with a CCC rating.

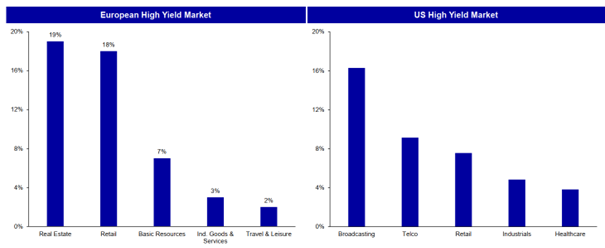

There are also differences regarding the sectors with the highest default rates. Defaults in Europe in 2023 were particularly in the real estate and retail sectors whereas bankruptcies in the US were more concentrated in the broadcasting sector, but also in the telecommunications industry and the retail sector5.

Major differences between Europe and the USA with regard to the sectors with the most defaults

Source: JP Morgan. As of December 29, 2023

In Europe, around 44% of high-yield bonds will mature by 2026, compared with just 20% in the US6. However, Kallestrup expects the maturity wall in Europe to converge with that on the other side of the Atlantic due to large-scale refinancing waves. He emphasizes that better rated issuers with low coupon bonds outstanding – issued as government rates were negative – prefer keeping them until maturity as these bonds need to be re-financed at much higher coupons today. It has turned the European High Yield markets into shorter-duration and as most bonds are refinanced one year ahead of maturity (depending on the non-call period) the pull-to-par effect can deliver decent returns despite issuers with an unsustainable capital structure will default.

Caution with real estate bonds

In terms of performance, most sectors performed well between the beginning of 2023 and the end of February 20247. In addition, most companies have become more cautious and have reduced their leverage. This was particularly true of companies in the transportation and consumer goods sectors, which were hit particularly hard by the coronavirus pandemic. Companies in financial services and the healthcare sector, on the other hand, have seen an increase leverage.

Kallestrup also prefers sectors that have good fundamentals and are less cyclical and has an overweight in services and underweight in automotive as well as basic industry. He also favors senior secured bonds with higher recovery rates. Furthermore, there is a preference for subordinated bank capital in systemically important banks in Northern Europe rather than smaller banks in Southern Europe. He is more cautious when investing in bonds from the real estate sector, which, depending on the region, is subject to substantial risks.

1https://www.morningstar.com/funds/6-top-performing-high-yield-bond-funds

2ICE BAML, Credit Suisse. As of: 31 December 2023

3JP Morgan Research, LCD. As of: 29 December 2023

4JP Morgan Research, LCD. As of 29 December 2023

5JP Morgan Research. As of: 29 December 2023

6ICE BofA. As of: 29 December 2023

7Capital Four, Bloomberg