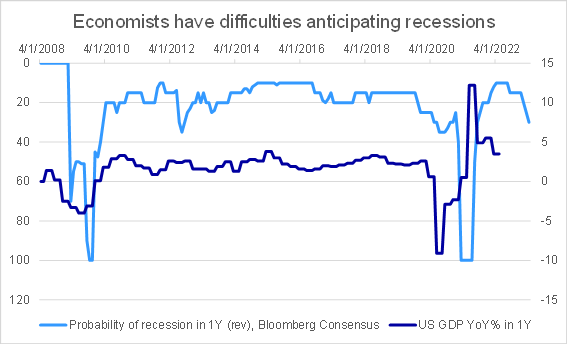

What did the ECB decide?

The ECB released its new economic forecasts on growth and inflation, justifying a cycle of monetary tightening. The ECB now points to a 25 basis point rate hike in July followed by a potentially large rate increase in September depending on the medium-term inflation outlook. Beyond this the ECB points to a gradual but sustained pace of rate hikes without any discussion on the terminal or neutral rate. Goldman Sachs for example now expects 2x25bp rate hikes and 2x50bp this year for a terminal rate of 1.75% next year which seems a reasonable view.

Quantitative Easing

The QE programs APP ends in July and the PEPP reinvestment will be used, in as much as it can, to deal with potential dislocations. The problem for the European periphery is that the ECB’s inflation forecasts are very elevated for 2022 (see table below). Hence, the ECB is only continuing a hawkish turn targeting a terminal rate that is as yet unknown and not easy to forecast as stocks such as real estate eventually adjust. That leaves the Italian and Greek curve open to fears that higher interest rates will lead to questions regarding debt sustainability especially as expected growth there is too low. As a consequence, the Italian 10 year BTP rose by 20bp on the back of the ECB’s decision to hike in July/Sept. Eventually, in a year or two if things go well, the ECB will likely reduce its balance sheet hurting again the prospects for the Italian and Greek curve. That leaves investors warry of holding long-dated peripheral bonds as a long-term investment though this might be tactically interesting.

Source: Nordea Investment Funds S.A. and ECB

Defragmentation

The ECB suggests it is working on tools to deal with fragmentation in the Eurozone at a time when the BTP 10 year curve is at a spread close to 250bp with Bunds when it last intervened. It is too early to privatize these purchases with a bank funding TLTRO whose terms will be less advantageous than in the past. The ECB could widen the access to the TLTRO to asset managers and pension funds but that would mostly take profits from banks. It could simply fund sovereign wealth funds and foreign reserves but only the largest ones such as Norway, Switzerland, China and Japan would invest in longer dated BTPs. More problematically, they would simply invest more into European credit and equity. What it boils down to effectively is that the ECB needs to convince the market that it can clearly forecast the terminal rate by winning the battle over inflation – which will take many months and force the ECB to be more hawkish, a turn that is unhelpful to BTPs.

EUR

As peripheral spreads widened on announcement day, EURUSD came under pressure, a feature that is likely to come back and this even as the ECB announced a cycle of rate hikes. The ECB needs a stronger EUR to deal with imported inflation and to avoid pressure from the US as it has devalued its currency amid a NATO proxy war with Russia. At the same time, they need the currency to stay somewhat weak to help exports, likely circa EURUSD 1.20 in the longer run. Initially, the market will likely continue to trade EUR as a credit proxy, but over time as the ECB tightens monetary policy and flows start to return to the periphery from abroad in the front-end, we should see EURUSD grind higher. As there should be few naked carry trades and fixed income is heavily hedged, the real mover for EURUSD flow wise should be foreign inflows into equities. That should happen when the European economy starts to recover in a few months, with European equities tilted towards cheap Value.

EURJPY is strengthening, led by a weaker Yen as the BoJ maintains its policy. The Yen continues to be an interesting tactical hedge in a risk-off environment but mostly against the USD.